Who’s Winning the Race?

Work Tech M&A Outlook

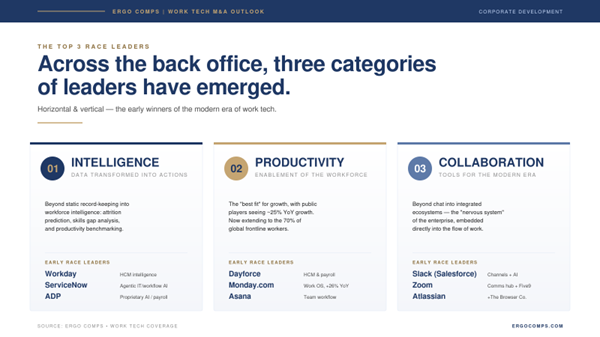

In the race to develop the next modern era of work tech solutions; whom are the early race leaders?

Across the backoffice - both horizontal and vertical - the top three (3) early race leaders feature

Intelligence. Data transformed into actions.

Productivity. Enablement of the workforce.

Collaboration. Tools for communicating and working in the modern era.

The race to develop the next era of work tech is a seismic market share realignment driven by digital transformation and massive capital deployment. With more than $25 billion in capital deployed in the since 2020 to fuel these investments, the industry is shifting from legacy administrative tools to intelligent, integrated ecosystems.

The recent transactions that closed reveal a market rewarding AI capabilities. Across the backoffice—both horizontal and vertical—three distinct categories of early race leaders have emerged.

Investment Trends and M&A themes & deal drivers for deals based on coverage of the new era of work tech across platforms, solution leaders, and niche leaders.

The current investment landscape for work tech is defined by valuation bifurcation – a K-Shaped economy has created K-shaped valuations -- and a focus on AI further expanding the split. A widening gap separates valuations into losers and winners, with top solutions and platforms command 10x+ EV/Sales and R-Values (Growth + EBITDA) greater than 50, while traditional software at 1x to 3x and services struggle at 1–3x multiples.

Key Deal Drivers

Strategic Buyer Dominance. Corporate strategic acquirers lead the M&A market

Premium for “Sticky” Revenue. Valuations are increasingly driven by Net Revenue Retention (NRR) and Gross Revenue Retention (GRR) metrics—demonstrating customer expansion potential and resistance to churn.

The Size Premium. Quality assets in the $10–50M ARR range command premium.

Platformization vs. Verticalization. Customers are demanding a one-stop-shop, consolidating point solutions into core systems of record. At the same time, niche industry specialists (speciality niche markets) are seeing 30%+ revenue growth, far outpacing industry generalists.

CIO/CLO Driven Mandates. Enterprises are shifting budgets from labor toward intelligent backoffice automation, fueling demand for “Everything-as-a-Solution” models that combine proprietary software with managed solutions.

The AI Mandate. Over the recent years, the majority of investment dollars are flowing to Agentic AI and Intelligent Automation.

The AI Readiness Gap. While AI is the primary deal driver, surveys indicate that a plan for AI disruption is the single area where target companies are least prepared for sale—creating a significant hurdle in due diligence.

Focus on Profitability. Profitability has become a critical gating item, as buyers prioritize operational fit and sustainable margins over leverage-driven bidding. Profitable growth (R-Value beyond Rule of 40 matters).

The race has just begun — with new AI capabilities, new business models, and new revenue pricing and solution delivery models,; early indication that there are new investment economics to consider.