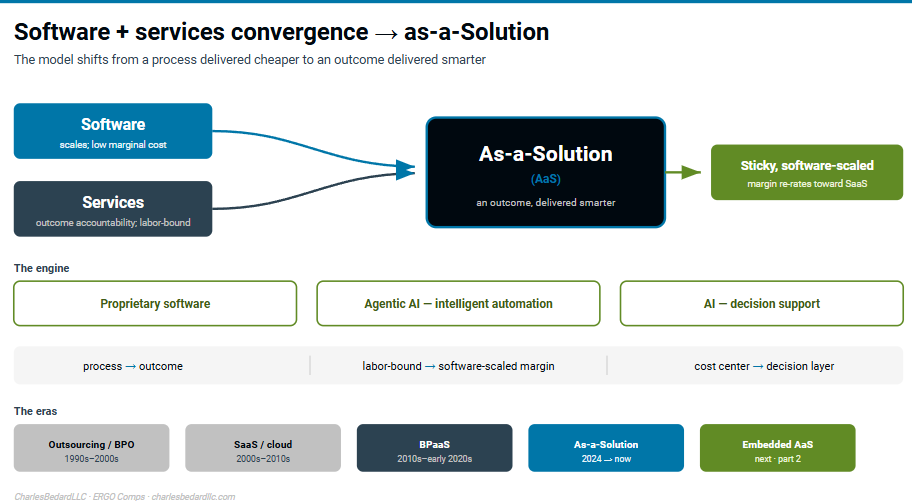

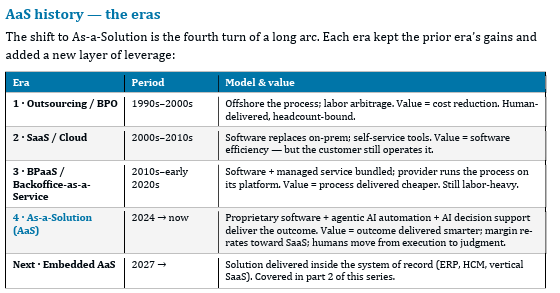

As-a-Solution: The Software & Services Convergence

The insight from the news monitoring

The headline

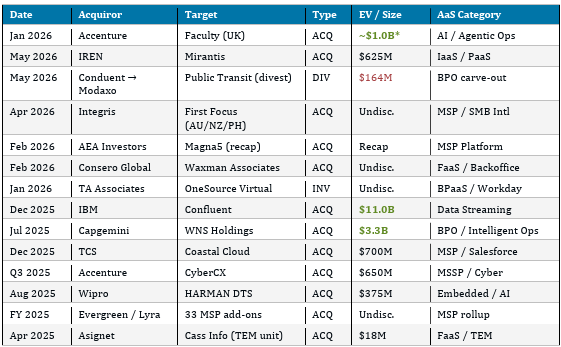

When software stops being a product and starts being an outcome, the buyers change — and so does the price. Across 2025 and the first half of 2026, the largest services and software acquirers spent to own one thing: the delivery layer between a customer and a result. My DealNet captures 50+ transactions and four signals fitting the As-a-Solution / As-a-Service pattern — the largest being TA Associates+OneSource (est $1B), Capgemini–WNS ($3.3B), IBM–Confluent ($11.0B), and Accenture–Faculty (~$1.0B). The thesis is no longer “buy software” or “buy services.” It is buy the converged solution.

The pattern

Three buyer archetypes are converging on the same target profile. Mega-cap IT-services firms — Accenture, IBM, Capgemini, TCS, Wipro, Cognizant — are buying AI-native and cloud-managed capability and wrapping it in managed delivery. PE-backed platforms — Evergreen/Lyra, Integris, AEA’s Magna5, Versaterm, Consero — are rolling up fragmented MSP, ERP-channel, and Finance-as-a-Service shops. And HCM / work-tech incumbents — Workday, SAP, Paychex, ADP, UKG — keep buying AI and workflow to defend the platform. The common denominator: recurring revenue delivered as a service solution today, with software and human expertise sold as one outcome.

The signal

Of 50+ deals, 12 are publicly disclosed ,but most of the volume is mid-market and undisclosed — the tell of a rollup cycle. Two structural signals reinforce it: legacy BPO is shedding non-core assets (Conduent’s $164M transit carve-out to Modaxo, plus a CEO and board reset that usually precedes more sales), and growth capital is re-entering Workday-services BPaaS (TA Associates’ majority growth investment in OneSource Virtual).

The deal table — consolidated AaS transactions

Observations

1. AI is part of the thesis

The marquee 2026 deals are AI-capability buys dressed as services. Accenture bought Faculty to own applied-AI delivery — its CEO became Accenture’s CTO. Cognizant bought 3Cloud for ~1,200 Azure specialists. IBM assembled Hakkoda, Neudesic, Cognitus, and Txture into a managed data/AI stack. Buyers are not licensing AI; they are acquiring the people and pipelines that turn AI into a billable outcome.

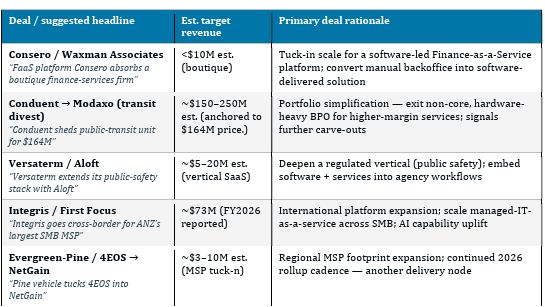

2. The vertical rollup is where the volume lives

Most deals carry no disclosed price because they are tuck-ins into PE platforms. Evergreen alone added 33 MSP businesses across five countries — Lyra hit $1B ARR in June 2025 — plus nine ERP-channel partners through its Pine vehicle. The price opacity is the point: these are route-to-revenue buys, not trophy assets.

“The platforms aren’t buying companies — they’re buying route-to-revenue. Every tuck-in is another delivery node.”

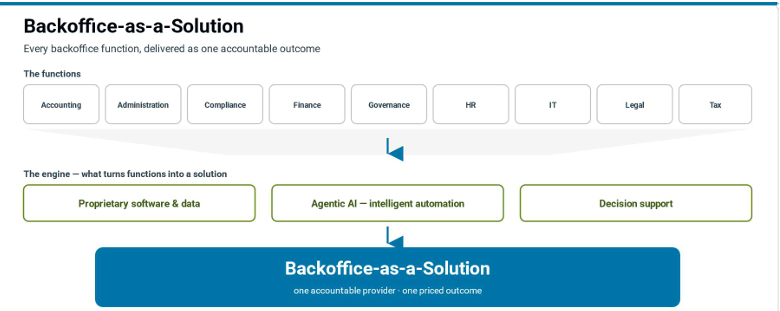

3. Backoffice-as-a-service is consolidating in plain sight

Finance- and payroll-as-a-service is quietly compounding: Consero added Waxman; MPAY/Payentry absorbed Corporate Payroll Services; Asignet bought Cass’s TEM unit ($18M). DealNet’s watchlist already flags 19 XaaS-tagged comps, weighted to Finance-as-a-Service and backoffice. The next platform fights are forming here, below the headline multiples.

The playbook lesson for corporate development: Stop sorting targets into “software” or “services.” Buyers are paying premiums for the converged delivery model — recurring revenue, embedded expertise, and an AI layer that lowers cost-to-serve. Index sourcing on delivery model and gross-margin trajectory, not on the label.

DealTalk Monitoring Signals Insights review of AaS Deals