The K-Shaped Market…Why Average is NOT Good Enough

Our USA K-shaped economy is driving K-shaped business financial performance, which is driving K-shaped valuation returns. Three drivers are widening the gap ….

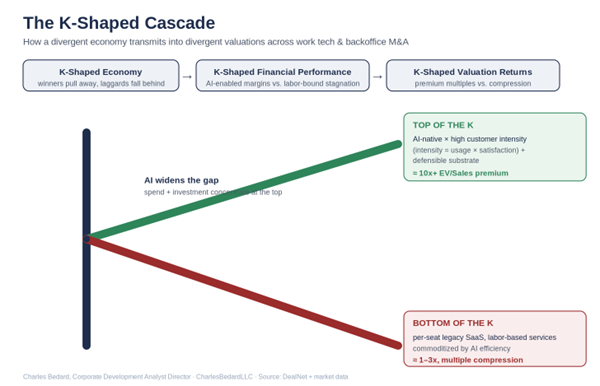

"K-shaped" entered the vocabulary to describe an uneven recovery - some racing ahead while others fell behind.

A market that once paid similar range of value multiples for similar-looking firms now pays radically different ones depending on which arm of the K a company sits on. Two businesses with identical revenue can sit a full order of magnitude apart on multiple. So the question every operator, buyer, and investor in has to answer is blunt: are you sliding up the K, or down it?

Driver 1 - AI as the strategic imperative

AI is the central force, and the only honest framing of it is a question: is your AI strategy a cost, a threat, or an advantage? In every credible read of the market, AI is the top driver - in DealNet, roughly a third of all 2024-2026 work tech transactions are AI-tagged by count, and market estimates put more than half of sector dollars flowing to AI-focused assets. The marquee deals make it concrete: ServiceNow's $2.85B acquisition of Moveworks, Salesforce's $8.0B purchase of Informatica, and Workday's run of AI tuck-ins (Sana Labs at $1.1B, Paradox at $1.0B).

But AI is not just being bought; it is splitting the market. Agentic AI is questioning the terminal value of traditional per-seat software - a handful of agents can now do the work that once justified the seats. What looks like enthusiasm for AI-native assets is, from the other side, a quiet repricing of everything that is not. AI-native pulls a company up the top arm of the K; per-seat legacy slides down the bottom arm. The same technology does both.

And the premium is not spiking for "AI" generically. It is spiking for specific solution categories - the ones that turn data into action and intelligence into outcome:

1. Sentiment and predictive analytics that listen, plan, predict, and act on what people, talent, and the workforce will do.

2. Data transformed into intelligence for workforce resource planning and advanced scheduling.

3. Orchestration that designs, builds, directs, governs, and optimizes intelligent automation - beyond RPA and ML - for agentic AI workflows.

4. The intersection of productivity and intelligence - tools that make people measurably more effective, not just better informed.

5. Outcome- and usage-priced AI solutions that are more effective contributors on day one than legacy apps - implemented at a fraction of the time and cost.

What unifies the list is a single test: the premium goes to innovative solutions that also drive meaningful customer intensity – the customer satisfaction multiplier.

Driver 2 - Platform vertical consolidation

The second driver is consolidation, but not the old kind. M&A has moved beyond expansion by product or market into "owning the stack" - the one-throat-to-choke logic in which customers demand a single integrated system for workflows, data, compliance, and payments rather than a drawer full of point solutions. Three moves define it.

Driver 3 - Flight to quality

Strong assets - high growth and margins - command significant premiums; average assets face steep valuation discounts.

What it means

These three drivers point the same direction: the market has stopped paying for the average. The category-average multiple - the number a generalist could once count on - is dead as an underwriting tool.

For operators, the only question that matters is which arm you are on?

The playbook for your situation depends on your K position.

Charles Bedard, Corporate Development Analyst Director at CharlesBedardLLC, covers software, solutions, and services across work tech and backoffice. Source notes. Deal-level data from DealNet (CharlesBedardLLC); deal values are disclosed or estimated transaction sizes. Market-level statistics - the share of sector dollars flowing to AI, the ~10x vs. 1-3x multiple split, and the above-average-performer premium - are drawn from market research compiled for this analysis and should be treated as directional. Representative transactions cited for illustration, not as a comprehensive deal set